Effectively hedging portfolios is a challenging task that involves a careful weighing of tradeoffs. Dedicated hedges can cushion a portfolio during times of stress, but they also tend to lose value quickly while markets rise. Low-correlation exposures such as Alpha Seeker have the ability to profit regardless of the direction of broad markets, but may not be perfectly anti-correlated during every market decline. With the right vehicles in the right combination, it may be possible to construct an exposure that retains most of the benefits of hedges while greatly reducing their cost.

July 2021 Commentary

Presently, VIX prices remain mostly higher than would normally be expected for a quiet equity market near all-time highs. So far, this has just been been another “wall of worry” for stocks to climb, but with the historically turbulent fall season and the Fed’s Jackson Hole symposium approaching, a change could be in store.

June 2021 Commentary

Equity markets were higher again in June, with recently-battered tech names roaring back relative to US small cap stocks. This resulted in a mostly sleepy VIX aside from a slight disturbance around the mid-month Fed meeting which hinted at sooner-than-expected rate hikes. Notably, treasury yields dropped on the announcement, apparently signaling a policy error that would choke growth

May 2021 Commentary

Chop chop

VIX Index May 2021

US equity markets flailed around the unchanged line for the most part in May, with the S&P 500 (+0.70% MTD) once again outpacing the tech-heavy Nasdaq 100 (-1.26% MTD) as growth and inflation expectations continue to rise. This ongoing rotation produced a jumpy, range-bound VIX and marginal signals from the dashboard, resulting in moderate hedging costs in TCM strategies and a down month for Alpha Seeker.

International markets fared better, as EAFE Smart Index (+1.92% MTD) and Emerging Markets Smart Index (+0.65% MTD) hover near 5-year highs. With its equity-based holdings and similar hedging expense to Smart Index, our new Hedged Yield strategy fell slightly (-0.60% MTD) in its first full month of trading, while currently producing a gross yield of 9.3%. Schedule a webinar with us to learn more.

on the right path

Correlation is a popular topic in finance, with investors and allocators often expressing a desire for low- or non-correlated exposures in their portfolio. However, in actually assessing these strategies the focus tends to quickly revert to total return as the yardstick for their inclusion in a portfolio. While total return is of course an important consideration, the potential benefit from a strategy’s path of return (its correlation) should not be overlooked.

The purpose of a non-correlated asset is not to add leverage, but to change a portfolio’s path of returns in a beneficial way. As an extreme example: at the right allocation, a non-correlated asset can improve a portfolio’s overall return even if the asset itself loses money! (see table below)

Hypothetical example for illustrative purposes only.

This is possible because of the different sequence of returns that results from adding the non-correlated asset. Since investment returns compound from year to year (this year’s returns are on last year’s ending value), even just changing the path of returns with a non-correlated asset can produce a benefit for a portfolio. In this case, Asset B’s preservation of capital during the market decline in year 2 produced a compounding benefit (more capital for the rally in year 3) that exceeded a small loss from the asset itself.

Of course, not all alternative assets are alike and there are the ever-present risks of allocation size, timing and psychological factors to consider. It’s not an easy task, but with the proper focus, it is possible to build more durable portfolios with an allocation to non-correlated assets.

April 2021 Commentary

steady as she goes

VIX futures prices, April 2021. Source: vixcentral.com. Click for larger image

Volatility continued to normalize as equity prices pushed higher in April, supported by strong earnings reports and ongoing accommodation from the Fed. Absent some turbulence around news of a Biden tax plan that would see capital gains rates at their highest levels in decades, a message of calm from the VIX meant positive beta exposures and positive returns for TCM portfolios throughout the month.

Benefitting from a “mini rotation” back towards growth names, Hedged Disruptor (+6.3%) and Smart Tech (+6.2%) led the way in April, while all other strategies saw continued gains including US Equity Smart Index (+5.6%) which now stands at +12.7% on the year vs +11.8% for the S&P 500, extending its lead on the index after an outstanding 2020. Not just a US phenomenon, each strategy in the Smart Index family is ahead of its benchmark on the year through April with less volatility.

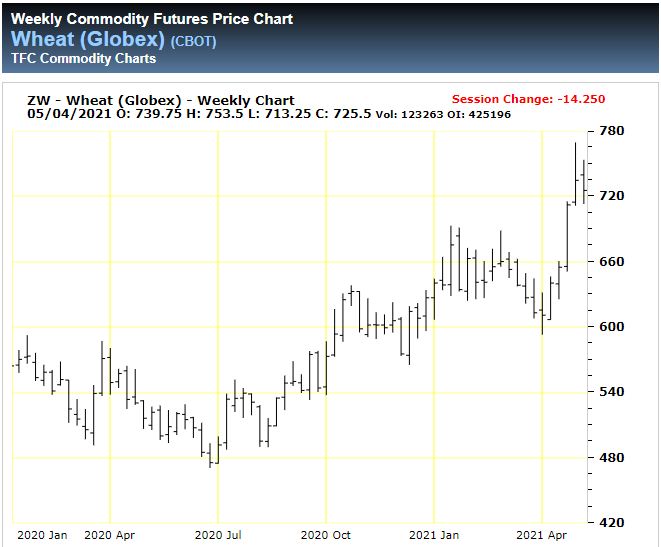

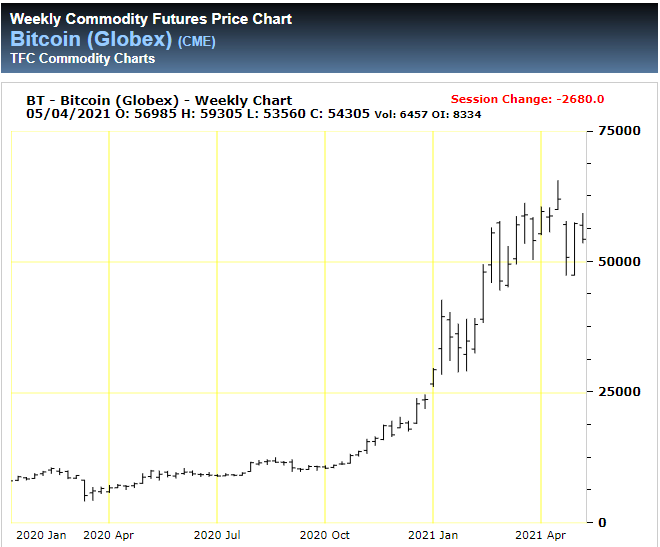

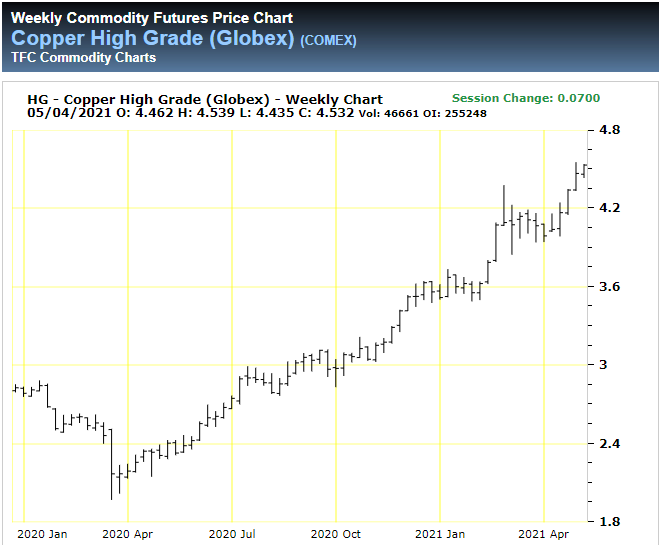

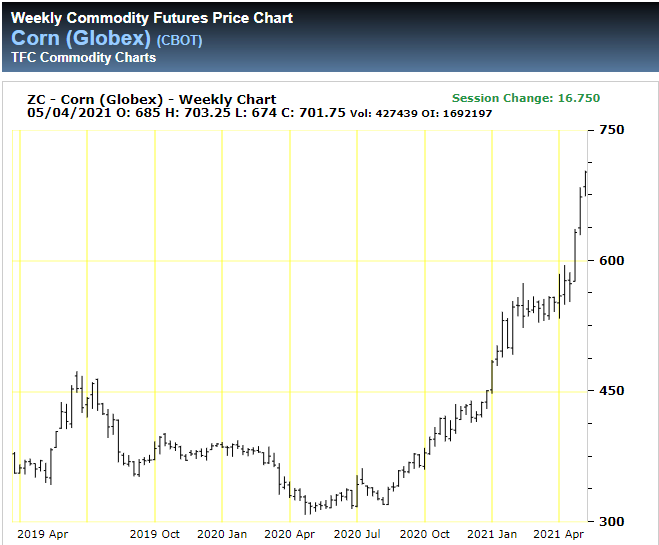

swarm of flies

As stocks continue to bask in the glow of highly accommodative monetary policy, a potential “fly in the ointment” may be on the horizon. While the Fed has repeatedly declared their willingness to temporarily let inflation run over their 2% target before raising rates, recent movements in many major commodities and alternative currencies (see gallery below) appear ready to test that statement.

As we saw earlier this year, even a mild rise in rates can cause major ripples in the equity markets of highly leveraged economies like the US. While Fed-induced episodes like in Q4 2018 can be reversed with a rate cut or two, containing an inflation-driven spike requires bold and difficult (ie, market-unfriendly) action that seems to be in short supply at today’s Fed.

This is simply an observation of one of the myriad of factors that might affect markets. Nobody (including us) knows if this will be “the” issue or even an issue at all for stocks, so we will remain focused on the message from the VIX to help guide us through whatever comes next.