Rotation nation

As interest rates hit a one-year high, markets continued to rotate away from large growth names in March, turning briefly violent as news of the forced liquidation of a heavily-leveraged Chinese fund made the rounds. By the end of the month most equity indexes finished higher, with smaller value exposure again benefitting at the expense of large cap growth.

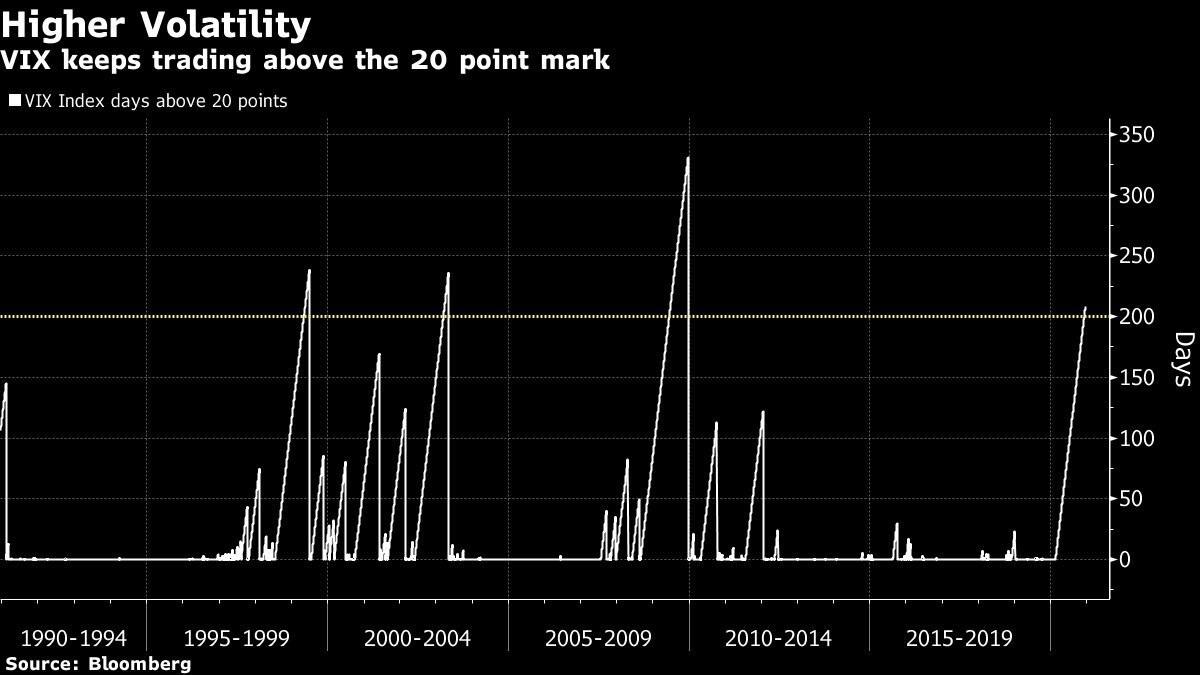

Since it responds to volatility expectations in the S&P 500 as a whole, a shuffling in the component sectors is rarely the recipe for a substantial rise in the VIX index. In fact, after some early strength the VIX fell -31% in March, potentially broadcasting an “all clear” signal as it settled below the key 20 level that has been a floor since the Corona Crisis began over a year ago. Accordingly, defensive positions were largely absent from TCM portfolios in March except for a brief appearance early in the month that weighed somewhat on performance. (see next section for more on TCM risk management)

March 2021 MTD return comparison. Source: Yahoo Finance

With the lone exception of Hedged Disruptor (-9.6% YTD) which has been weighed down by the ongoing rotation from growth, 2021 is off to a strong start at TCM with Alpha Seeker (+9.5% YTD) leading the way and all Smart Indexes ahead of their benchmarks on the year. As the economy reopens and the VIX tentatively exits the “crisis formation” that has been in place for over a year, the market appears ready to move on from this crisis and begin searching for the next one.

On precision

TCM’s risk management philosophy is to lessen the effect of crisis periods by basing its equity exposure on signals from the VIX. A quantitative system might imply a certain level of precision, but ultimately the Volatility Dashboard tracks human emotion which is far from precise. The success of TCM portfolios is therefore not the result of superior accuracy, but of convexity. In other words, investor behavior is difficult to predict but when it becomes irrational, it can become very irrational.

In practice, this means that the majority of TCM’s hedging positions are expected to be unprofitable, with the less frequent profits outstripping more common losses. Indeed, as of March 2021, 58% of hedging trades in US Equity Smart Index have been unprofitable, subtracting an average of -0.75% from performance on all days when they have been present in the portfolio. On the other hand, less frequent profitable hedges have added an average of +1.51% to the portfolio on days when they have been used, including an astounding +19.1% during “Volmageddon” on 2/5/18 and +12% to +14% contributions on three separate days during the March 2020 “Corona Crisis”. This is convexity, and it can be powerful when used correctly.

US Equity Smart Index sample account daily hedge attribution, Nov 2016 - Mar 2021. Source: TCM